Health insurance has become an essential part of financial planning in India. With rising medical costs and increasing health risks, having a reliable health insurance policy ensures peace of mind and security for you and your loved ones. However, choosing the right plan can be challenging, especially as regulations and coverage options evolve over time. This article will guide you through the key updates for 2023–2024, the expected trends for 2025, the latest Insurance Regulatory and Development Authority of India (IRDAI) guidelines, and new mandatory coverage items—so that you can make an informed decision when selecting your health insurance plan.

Escalating Medical Costs

Medical inflation in India has outpaced general inflation in recent years. By 2025, healthcare costs for hospitalization, surgery, and specialist consultations are likely to be even higher. A comprehensive health insurance plan can shield you against steep medical bills and allow you to focus on recovery.

Greater Awareness of Preventive Care

More Indians are recognizing the importance of preventive healthcare, such as regular check-ups, diagnostic tests, and early interventions. Many newer policies cover preventive care benefits, which can reduce the need for more expensive treatments down the line.

Inclusion of Advanced Treatments

The medical landscape is advancing rapidly, with new procedures like robotic surgeries, advanced radiotherapy, immunotherapy, and precision medicine becoming more common. Health insurance plans increasingly cover these treatments, offering policyholders broader coverage.

Post-Pandemic Health Priorities

The COVID-19 pandemic shed light on the importance of having a robust health insurance plan. Even as the pandemic wanes, new variants or other infectious diseases could emerge, making comprehensive health coverage more crucial than ever.

Mental Health Coverage

Telemedicine and Digital Health

Additional Coverages

The IRDAI (Insurance Regulatory and Development Authority of India) regularly issues guidelines aimed at improving transparency, affordability, and accessibility in the health insurance market. Below are some key points from the latest directives that are either in effect or expected to come into force by 2025:

Standardization of Policy Wordings

To reduce ambiguity, IRDAI has pushed for standard definitions and terms in policy documentation. This includes uniform terminology for exclusions, waiting periods, and sub-limits, making it easier for customers to compare plans from different insurers.

Mandatory Coverage Additions

Simplified Claim Settlement

A key focus for IRDAI is to simplify and expedite the claim settlement process. This involves stricter timelines for claim settlement and the adoption of digital platforms to handle claims quickly and transparently.

Enhanced Portability

Health insurance portability allows you to switch insurers without losing accumulated benefits (like waiting period credits). IRDAI’s new guidelines emphasize smoother portability processes, ensuring minimal disruptions if a customer decides to change their insurer.

Greater Transparency on Network Hospitals

Insurers are required to maintain an updated list of network hospitals and disclose any changes promptly. This initiative aims to help policyholders easily identify network hospitals and avoid out-of-network costs.

In addition to mental health and telemedicine, here are some other coverage areas that have become mandatory or are expected to become mandatory by 2025:

Preventive Screenings

Insurers must include certain mandatory annual or biennial health check-ups for policyholders, encouraging early detection of conditions like diabetes, hypertension, and cancer.

OPD and Day-Care Treatments

With medical technology enabling more procedures to be completed within a few hours, coverage for day-care treatments is expanding. Some policies also include OPD expenses, minimizing out-of-pocket costs for routine medical needs.

Maternal and Newborn Care

Several insurance providers now include mandatory coverage for maternity-related expenses, neonatal care, and newborn screening within standard family floater plans, though sub-limits may apply.

Emergency Road and Air Ambulance

As medical emergencies can require rapid transport, IRDAI has encouraged insurers to include coverage for ambulance services, including air ambulances in critical cases, to ensure timely medical assistance.

When selecting a health insurance plan in 2025, you should look beyond just the premium amount. Here are critical factors to keep in mind:

Sum Insured vs. Medical Inflation

Opt for a sum insured that will remain sufficient against projected medical costs in the next few years. With expenses rising, a higher coverage limit might be prudent, especially for families.

Coverage of Critical Illnesses

Verify if the policy covers life-threatening conditions like cancer, heart ailments, kidney failure, and other critical illnesses. Some insurers offer riders (add-on covers) specifically for critical illnesses at a nominal increase in premium.

Network Hospitals

A vast and reputable network hospital list can be incredibly beneficial. Cashless treatment in a network hospital spares you the burden of paying out of pocket and then filing for reimbursement.

No-Claim Bonus (NCB)

Many insurers offer a No-Claim Bonus, which increases your sum insured by a certain percentage if you don’t make any claims during a policy year. This can significantly enhance coverage over time without large hikes in premium.

Co-Payment, Deductibles, and Sub-Limits

Waiting Periods

Policies often have waiting periods for pre-existing conditions or specific treatments like maternity. Shorter waiting periods are more beneficial, especially if you have a chronic condition.

Claim Settlement Ratio

Check the insurer’s claim settlement ratio and reviews. A high ratio and positive feedback from existing customers indicate reliable claim processing, which can be crucial when you’re already dealing with a health crisis.

Additional Benefits and Riders

Look out for riders that can expand coverage—such as personal accident covers, critical illness riders, hospital daily cash, and top-up policies. These might be cost-effective ways to enhance your policy’s scope.

Compare Policies Online

Many insurance aggregator websites allow you to compare premiums, features, and network hospitals side-by-side. This can save time and help you make an informed decision.

Read Policy Documents Carefully

While standardized terms are improving, it’s still essential to read the fine print. Pay extra attention to exclusions, waiting periods, sub-limits, and claim processes.

Keep an Eye on IRDAI Announcements

IRDAI frequently updates guidelines. Stay informed through their official website, reputable news outlets, or your insurer’s customer portal. Knowledge of new rules can help you capitalize on better coverage or lower premiums.

Renew on Time

Lapses in policy coverage can lead to loss of continuity benefits (like waiting period credits). Set reminders for yourself to renew your policy on time. If you’re dissatisfied with your current insurer, consider porting to another provider rather than letting the policy lapse entirely.

Maintain a Healthy Lifestyle

A healthy lifestyle can directly or indirectly lower your premium costs. Some insurers offer wellness or reward programs, awarding points or discounts for completing fitness challenges, health screenings, or participating in health workshops.

By 2025, the health insurance sector in India is set to become more customer-centric, transparent, and inclusive:

Conclusion

Selecting the best health insurance plan in India for 2025 involves balancing your budget with your current and future healthcare needs. Stay updated on IRDAI guidelines, especially regarding mandatory coverage items like mental health and telemedicine, as these changes can significantly enhance your coverage. Look beyond the premium to examine benefits such as no-claim bonuses, network hospitals, claim settlement ratios, and additional riders that align with your personal or family’s healthcare requirements.

Whether you’re a first-time buyer or looking to renew an existing policy, diligent research and comparison will go a long way in ensuring that you have a plan which not only meets but exceeds your expectations. With healthcare advancing at a rapid pace—and costs following suit—a comprehensive health insurance policy can safeguard your well-being and financial stability for years to come.

US-India Deal Approaches: What President Trump’s Tariff Retreat Means for Bilateral Trade

US-India Deal Approaches: What President Trump’s Tariff Retreat Means for Bilateral Trade

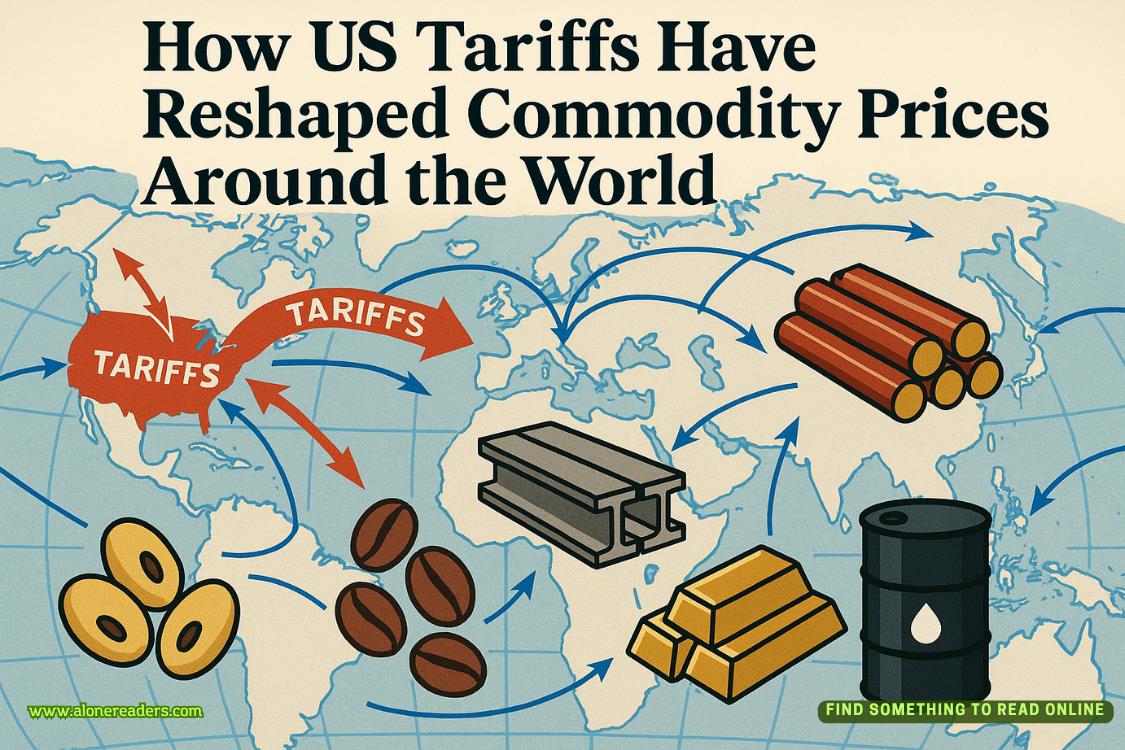

How US Tariffs Have Reshaped Commodity Prices Around the World

How US Tariffs Have Reshaped Commodity Prices Around the World

Sustainable Investing: Good for the Planet and Your Wallet

Sustainable Investing: Good for the Planet and Your Wallet

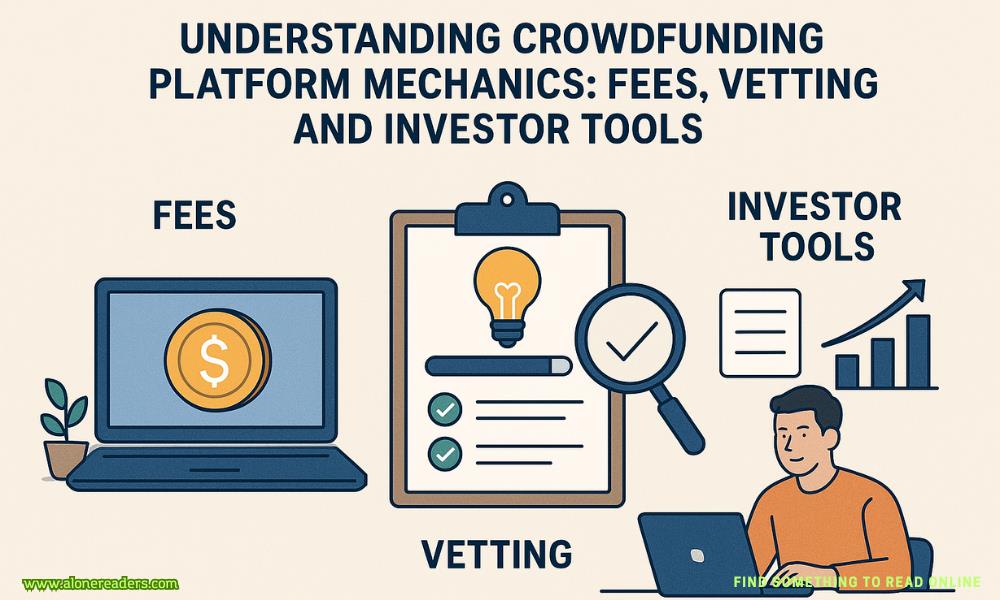

How Crowdfunding Platforms Work: Fees, Campaign Vetting, and Investor Tools

How Crowdfunding Platforms Work: Fees, Campaign Vetting, and Investor Tools

From Investment to Exit: Realistic Returns and Exit Strategies in Crowdfunding

From Investment to Exit: Realistic Returns and Exit Strategies in Crowdfunding

Risk Management in Crowdfunding Investments: Red Flags, Founder Vetting, and Smart Diversification

Risk Management in Crowdfunding Investments: Red Flags, Founder Vetting, and Smart Diversification